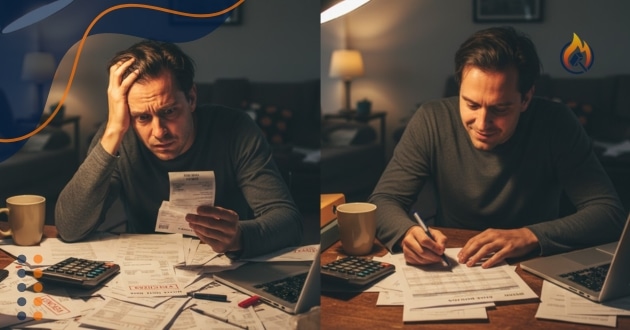

How to manage financial stress is necessary for your well-being in Canada. Many face concerns about personal finances, which even surpass work, health, or relationship stress. However, your money stress affects all these areas.

Research indicates that more than half of those living in Canada feel anxious about their money. This anxiety is not just psychological; it manifests physically. 49% of Canadians report losing sleep due to monetary concerns.

As a rule, financially stressed people are four times more likely to suffer from sleep problems and headaches. In addition to twice as likely to report poor general health.

Therefore, understanding how to manage financial stress is vital. Constant tension is associated with more severe health consequences, such as heart disease, hypertension, and worsening mental health, increasing anxiety and in some cases leading to depression.

This article will guide you through the strategy for managing financial difficulties. We will focus on practical actions and Canadian resources. Giving you the control you need to manage this.

Financial Stress as a Well-being and Productivity Crisis

Financial stress has established itself as the main problem linked to well-being in Canada.

For a significant portion of residents, this concern is the biggest source of tension, surpassing tensions related to personal health and interpersonal relationships.

Stress management transcends mere monetary advice. Positioning itself as a public health imperative.

The cost of financial stress also extends to the workplace. More than half of Canadian workers admit that personal finance concerns negatively impact their work performance.

Feelings of shame, guilt, and embarrassment lead people to isolate themselves. Staying only thinking about their financial problems.

However, communication, whether with a partner, a friend, or a professional, is one of the most effective methods to relieve this pressure and gain a new perspective.

The simple act of verbalizing the concern can deflate the perceived magnitude of the problem, being a crucial first step in how to manage financial stress.

Step by Step to Manage Financial Difficulties

The strategic management of financial difficulties begins with a logical and structured approach, focused on both mental well-being and practical action.

1. The Financial Diagnosis (How to manage financial stress)

The starting point is to gain total clarity about the current situation.

This requires mapping, identifying all sources of income, expenses (fixed and variable), the total amount of savings, and debt details.

To ensure accuracy, you should collect and review recent pay stubs, bank statements, and invoices.

Indeed, this phase is crucial for identifying essential fixed expenses (such as rent, mortgage, food, and insurance). Allowing the realistic calculation of an emergency fund goal, which economists suggest should be approximately six months of these expenses.

2. Budget Construction and Implementation

The budget is the map in times of difficulty.

It should be a living document, used to limit spending to what is planned. The Government of Canada offers very useful tools, such as the Budget Planner from the Financial Consumer Agency of Canada (FCAC).

This tool helps with data entry. Thus, you can compare your spending patterns with Canadian averages and provides personalized suggestions for next steps.

3. Start attacking debts (How to manage financial stress)

The next phase requires creating breathing room in finances.

This is achieved by reducing variable expenses and implementing a debt repayment plan.

Therefore, it is vital to avoid taking on more debt, as this intensifies the stress cycle.

If there are difficulties in making payments, inaction is the greatest risk.

We recommend immediately contacting the financial institution or creditors.

Communication with creditors about mortgages or credit cards can lead to temporary arrangements. Thus, it prevents the situation from worsening.

Indeed, we can help you lower your household bills. Through tips for reducing household expenses.

4. Seeking Professional Support in the Canadian Ecosystem

The Canadian financial ecosystem offers several layers of support.

- Credit Counselors: Non-profit organizations, such as those accredited by Credit Counselling Canada, offer free advice on debt management, budgeting, and financial education. They can help structure Debt Management Plans (DMPs). In addition to acting as the first line of defense against financial difficulties.

- Licensed Insolvency Trustees (LITs): If the debt is too large, LITs are the only professionals in Canada authorized to administer formal debt relief solutions. Seeking an LIT is the fastest way to break the cycle of stress, as the formal process offers legal protection against debt collectors and lawsuits.

5. Focus on Mental Health and Self-Care

Given the link between financial stress and mental health, self-care should be a priority.

It is essential to resort to support networks (friends, family) or mental health professionals for guidance and emotional support.

3 Extra Income Sources to Get Out of Debt

Increasing income through an extra income source is a way to accelerate debt repayment and reduce stress. Let’s look at the main jobs you can do:

- Digital Freelance Services and Consulting: Freelance work is flexible and can be done remotely. Platforms like Upwork, Fiverr, and Freelancer connect individuals to projects that use specialized skills, including web development, graphic design, writing, or business consulting. Use the skills you already have to earn extra money and get out of debt;

- Ridesharing and Delivery: Platforms like Uber Eats, Skip The Dishes, or ridesharing services have highly flexible schedules that can fit into busy agendas. Without a doubt, the money you earn from these services will help you a lot;

- Declutter and Sell Unused Items: Selling used items is a quick source of income to raise capital and free up space. Platforms like Facebook Marketplace, Kijiji, and Poshmark are popular for reselling clothes, shoes, and accessories in good condition.

Conclusion (How to manage financial stress)

Understanding how to manage financial stress is necessary to preserve health and quality of life in Canada.

Financial stress is not limited to numbers on a spreadsheet. It affects sleep, mood, and even work performance.

Managing this pressure requires a rational and emotional approach.

In practical terms, financial diagnosis and the creation of a realistic budget are fundamental steps to regain control. Psychologically, recognizing anxiety and seeking support whether from friends, family, or professionals is an act of courage and self-care.

Canada offers a wide support network, from credit counselors to accessible mental health programs. Adopting these strategies transforms money from a source of fear into an instrument of stability, promoting well-being, productivity, and lasting financial tranquility.